As the pace of the energy transition unfolds, Simon Flowers – Chairman, Chief Analyst and author of The Edge – claims that the speed of this transition continues to be the biggest uncertainty for strategic planning in the oil and gas industry. Following the signing of the Paris Agreement in 2015, it was easy to target net-zero by 2050 and depict a smooth 1.5 °C pathway on paper, but in reality, the road to a 21st-century energy mix was always going to be bumpy, as demonstrated by the Ukraine crisis.

Wood Mackenzie underlines that Tom ElIacott and Luke Parker, senior Corporate analysts, have shared the team’s thoughts on how Big Oil’s strategies are adapting to the challenges and changes on the road to net-zero. The firm says that the first step was strategic divergence, as the oil majors’ initial approach to decarbonisation after the Paris Agreement was shaped by stakeholders, not least government policy. At the time, Washington was indifferent to the Paris goals, tacitly giving the U.S. oil majors freedom to stick to what they knew best, as they focused on oil and gas.

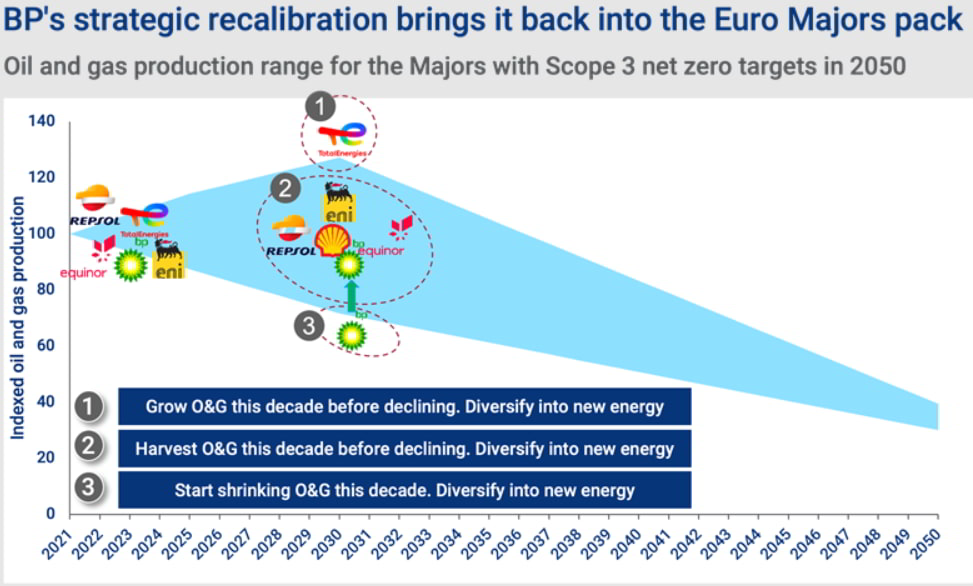

In contrast, Flowers underscores that the European oil majors mirrored the much more proactive and aggressive European policy response to pursue net-zero. In addition, the investors were highly influential in pushing for a decarbonisation agenda, as they responded to the burgeoning appetite for ESG investment. As a result, setting net-zero Scope 3 targets by 2050 implied a massive reduction in European oil majors’ oil and gas production and refining output from current levels.

Despite this, individual corporate strategies varied. While Shell set the initial corporate template for net-zero ambition that acted as a guide for the rest of the sector, BP positioned itself as a fast mover, more aggressive in committing to low-carbon investment, and more aggressive in committing to cut exposure to oil and gas. On the other hand, TotalEnergies has pursued a dual-pronged approach aiming to grow both, at least through 2030, regarded as a key marker on the global path to net-zero and as an inflexion point for many oil and gas companies.

Furthermore, Wood Mackenzie underscores that within the second step, strategies began to converge with the Ukraine crisis being a major factor, as governments have been forced to put energy security at the top of the agenda, above sustainability. Therefore, more oil, gas and coal was seen as the only way to keep the lights and heating on in the short run. As investors aligned with this strategy, the pressure on oil and gas companies has, for the time being, eased.

The energy intelligence group believes that another reason for investors’ more positive stance is that oil and gas companies are generating cash flow from upstream beyond their wildest dreams, thus, capital investment in oil and gas projects looks more attractive, albeit tempered by the still very real threat of declining oil and gas demand next decade and beyond. As a result, any incremental investment in oil and gas will continue to be in “low-cost, short-cycle, fast-payback projects with a below-average emissions footprint,” explained Flowers.

While the typically more modest returns from renewables and other low-carbon technologies haven’t necessarily deteriorated, Wood Mackenzie emphasises that the relative risk/return gap between upstream and renewables has widened, in the near term, at least, thus, capital allocation should shift towards upstream.

In lieu of this, the firm points out that the industry guidance for upstream capital investment in 2023 is up 15 per cent year-on-year and BP dialled back its aims to reduce oil and gas production and Scope 3 emissions to 2030 in an ad-hoc strategy update last month, moving from being an outlier to having an outlook closer to its other peers.

At the other end of the spectrum, the U.S. oil majors have continued to steer clear of committing to Scope 3 emissions reductions, giving them more room for manoeuvre, perhaps even to grow upstream. Although, they have started to dip their toes into low-carbon technology focusing on CCUS, renewable hydrogen and low-emissions fuels. Additionally, some European oil majors have throttled back from the breakneck accumulation of the renewables pipeline.

Regarding the third step, Wood Mackenzie forecast that the future is more convergence, as the world is still headed towards net-zero in the long term and so is Big Oil. By the next decade, the company predicts that energy security will be much more aligned with sustainability goals, shifting away from fossil fuels to domestically produced low-carbon energy and supporting supply chains.

Moreover, the energy intelligence group notes that policy initiatives in 2022 reinforce rather than undermine strategic positioning towards lower carbon business models beyond 2030 with Europe’s more aggressive targets and the game-changing tax incentives in the U.S. Inflation Reduction Act seen as key. Thus, the U.S. oil majors could significantly accelerate investment along the low-carbon technology value chain.

Meanwhile, Flowers says that the European oil majors’ share price ratings have traded at a big discount to their U.S. peers, even those that have demonstrated value creation in their initial renewables investments. Therefore, Wood Mackenzie concludes that convergence may help the European oil majors narrow the valuation gap. The firm sees BP’s sector-beating 15 per cent share price jump on its 4Q 2022 strategic update as a sign of changing investor sentiment.